What If a Rate Drop Costs You More?

March 26, 2026 | Buying

(3 Min Read)

Interest rate cuts are getting a lot of attention lately!! As borrowing costs start to ease, many buyers are thinking about getting back into the market and reconsidering homeownership.

Over the past few years, rising interest rates made it harder for people to qualify for mortgages. At the same time, home prices stayed relatively high, which caused a lot of buyers to pause their plans.

Now that rates are starting to trend downward, confidence is slowly returning. Lower borrowing costs can make monthly payments feel more manageable, and many buyers are beginning to see opportunities again.

But there’s something that often gets overlooked in this conversation.

Lower Rates Often Push Prices Higher

When interest rates fall, borrowing becomes more affordable. That means more buyers are able to qualify for mortgages and jump back into the market. And when more buyers enter the market at the same time, competition usually increases. More competition often leads to higher home prices.

Let’s look at a simple example.

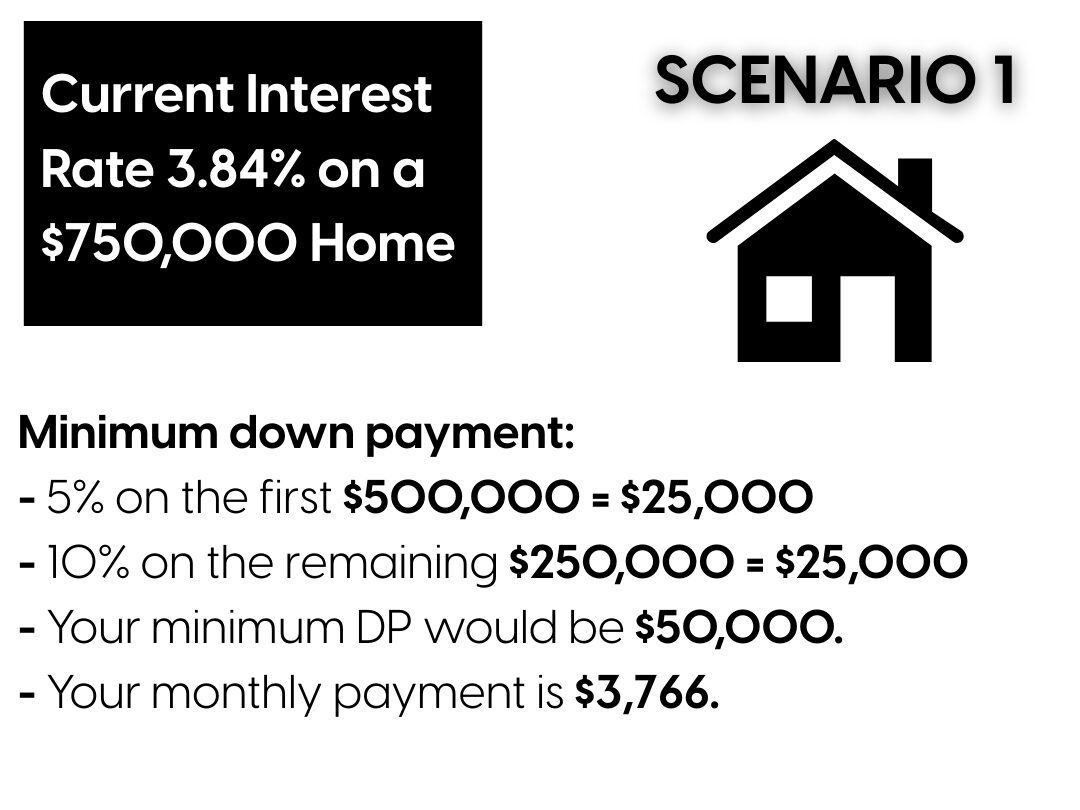

Imagine purchasing a home for $750,000. In Canada, the minimum down payment works like this:

– 5% on the first $500,000 = $25,000

– 10% on the remaining $250,000 = $25,000

– Your minimum down payment would be $50,000.

– With a mortgage rate of 3.84%, your monthly payment might be around $3,766.

Not bad… but you might be thinking “it could be worth waiting to see if rates drop a little more”.

When Waiting Backfires

Now imagine interest rates drop to 3.59%. That sounds like great news.

But remember, when rates drop, more buyers usually enter the market. As competition increases, sellers often feel more confident raising their prices.

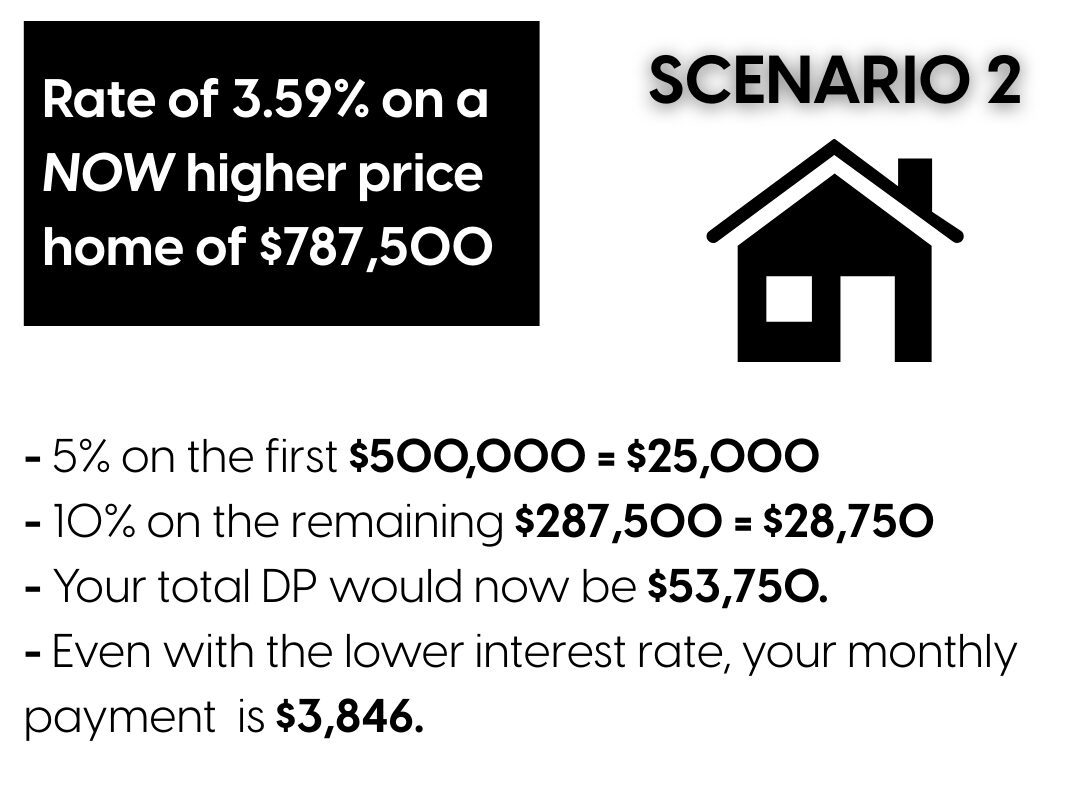

Let’s say that same property is now priced at $787,500. Your down payment would now look like this:

– 5% on the first $500,000 = $25,000

– 10% on the remaining $287,500 = $28,750

– Your total down payment would now be $53,750.

– Even with the lower interest rate, your monthly payment could be around $3,846.

So what changed?

You now need $3,750 more upfront

Your monthly payment increased by about $80

The property price increased by $37,500 (loss in equity)

In this situation, the lower rate didn’t actually save you money.

Buying Power Matters More Than Perfect Timing

Interest rates are only one part of the equation. Home prices, competition, and demand all play a role in overall affordability.

When rates drop, more buyers tend to enter the market at the same time, and prices can move quickly.

That’s why trying to perfectly time the market doesn’t always work the way people expect. In some cases, buying when rates are slightly higher but prices are lower can actually put you in a stronger financial position. You secure the home at a lower price and start building equity sooner.

….And if rates drop later, refinancing is always an option.

Waiting for the “perfect” interest rate might seem like the safer move, but in many cases it can actually reduce your buying power.

The right time to buy is less about perfectly timing the market and more about finding the right opportunity when it makes sense for your situation.

Let us help you get there faster and smarter!

Let us help you get there faster and smarter!